Boost Your FICO Score: 10 Effective Strategies for Improvement

Written on

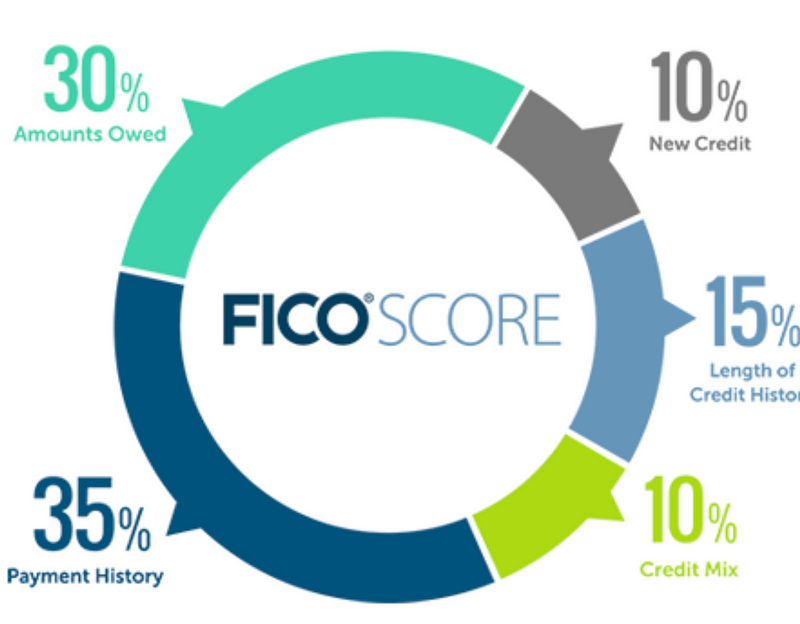

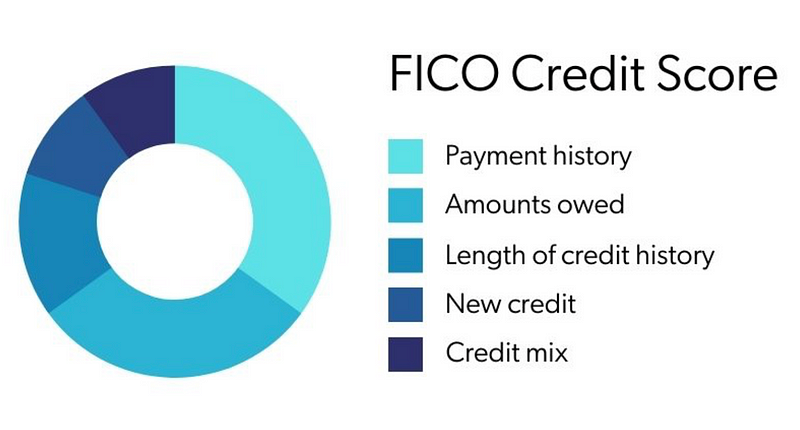

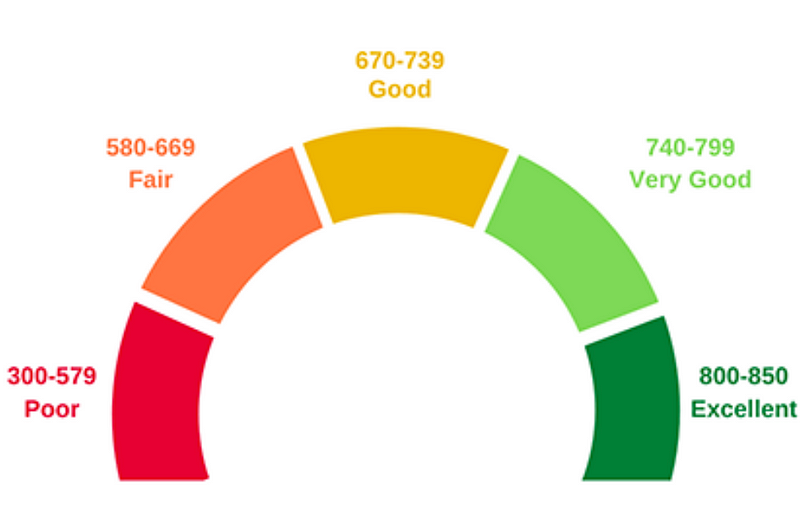

Understanding Your FICO Score

Improving your FICO score is crucial for financial health and can open doors to better credit options. Here are ten effective strategies to enhance your credit score.

"Engaging with this content can significantly enhance your understanding of credit management."

Section 1.1 Obtain a Credit Card Early

To secure your own credit card, you typically need to be at least 18 years old. However, you can also become a co-owner of a card with someone you trust—like a family member or friend—who has a solid credit history and maintains a zero balance. Choose someone reliable and not facing financial troubles.

Subsection 1.1.1 Piggybacking for Better Credit

One method to boost your credit score is "piggybacking." This involves getting added as a co-owner on someone else's credit card. Look for a cardholder who has: a) A high credit limit b) Utilization below 15% c) A strong, trustworthy credit history

As the primary account holder, it’s wise to keep control over the card until you fully trust the co-owner's spending habits.

Section 1.2 Keep Your Credit Utilization Low

Aim to keep your credit utilization ratio under 30%. For example, if your card limit is $2,500, try to maintain a balance between $0 and $750. A lower ratio is even better, ideally between 0% and 15%.

Chapter 2 Strategies for Credit Improvement

The first video titled "How To Increase Your Credit Score in 4 Days | Improve Your Credit Score by 100 Points" provides valuable insights on rapidly boosting your credit score through strategic actions.

The second video titled "How to INCREASE Your Credit Score FAST (Beginner's Guide)" offers a beginner-friendly approach to enhancing your credit score quickly.

Section 2.1 Increase Your Credit Limits

Raising your total credit limit can positively influence your score, especially if you have to carry debt. For instance, if Jane has a $25,000 limit with only $300 charged, her utilization is just 1.2%, presenting her as a low-risk user. Conversely, Jenny with a $2,500 limit and the same charge has a 12% utilization ratio, which is viewed as average.

Note that while increasing limits can help, self-control is vital. Avoid overspending just because you have a higher limit. You can request credit limit increases every six months, but keep in mind that credit inquiries can affect your score.

Section 2.2 Maintain Card Activity

Many rewards or store cards require regular use to remain active. Be aware of the potential for automatic cancellations if you don't use your cards regularly.

Section 2.3 Keep a Small Balance

Surprisingly, maintaining a small balance—like $20—on your credit card can positively influence your credit score. Banks prefer seeing some activity, as they earn interest on outstanding balances. Therefore, keeping a small balance can be beneficial.

Section 2.4 The Importance of Card Age

The longer you hold a credit card, the better it is for your score. Older cards demonstrate stability and reduce perceived risk to lenders. This is why it's advantageous to acquire credit cards early, even before turning 18.

Section 2.5 Diversify Your Credit Portfolio

Having a mix of credit types—credit cards, store cards, mortgages, and auto loans—can positively impact your FICO score. A varied credit portfolio, maintained at low balances, indicates to lenders that you are a responsible borrower.

Section 2.6 Avoid Canceling Credit Cards

Be strategic when considering canceling a credit card. Closing accounts can lower your average credit age and increase your perceived risk. It's advisable to keep high-limit cards open unless there’s a compelling reason to close them.

In conclusion, these essential tips can help you enhance your credit score and ensure you demonstrate responsible credit management. Stay informed and proactive to achieve the best FICO score possible.